Just 38.5% of Annual Nature Finance Needs Are Met, but UNEP’s New Report Tells a Story of Hesitation, Not Failure

Photo Copyright © Karunakaran Parameswaran Pillai/TNC Photo Contest 2021

This article updates a previous Nature4Climate piece on the UNEP State of Finance for Nature figures. It reflects new data from the 2026 edition of the report, which tracks 2023 finance flows.

We need nature-based solutions to help tackle the intertwined crises of climate change, biodiversity loss and land degradation. The good news is that investment in these solutions is still moving in the right direction. The bad news is that it is not moving nearly fast enough.

Read more

Related articles for further reading

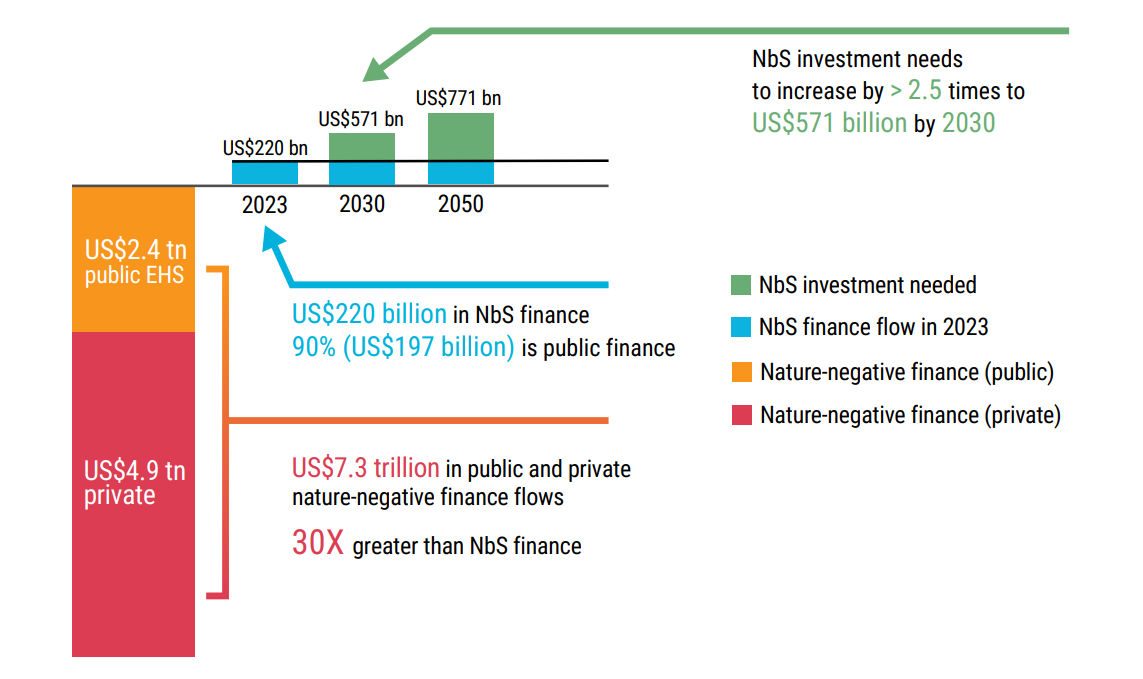

According to UNEP’s latest State of Finance for Nature report, nature-based solutions received roughly US$220 billion in 2023. That is up from US$200 billion in 2022. But the pace of growth has slowed. After rising 11% in the previous assessment, finance grew by just 5% this time around. And while the total is moving closer to what is needed, it still amounts to only 38.5% of the annual US$571 billion required by 2030 to meet global climate, biodiversity and land goals.

So, are things improving? Yes. Are we on track? Not yet.

A few years ago, we wrote that nature-based solutions were receiving only 37% of the finance needed to reach global climate goals. That figure helped show just how large the gap was, and how far nature remained from the center of global investment. The new numbers tell a slightly more encouraging story, but only slightly. The gap is narrowing, but slowly. The target has shifted from roughly tripling finance to scaling it by around 2.5 times. That is an improvement. But it is still a daunting challenge, especially when momentum appears to be weakening at precisely the moment it should be accelerating.

BETTER ANALYSIS

As with previous updates, part of what has changed is the quality of the underlying data. UNEP’s State of Finance for Nature report has continued to refine its methodology and broaden its scope. It now offers a clearer picture not only of how much is flowing into nature-based solutions, but also of how much finance continues to flow in the opposite direction.

That bigger picture matters. In 2023, finance directly harmful to nature reached US$7.3 trillion. That is more than 30 times the amount flowing into nature-based solutions.

In other words, even as investment in nature continues to rise, the global economy is still overwhelmingly financing the destruction and degradation of the very systems it depends on.

This is one of the most important insights in the new report: that harmful finance still dwarfs positive finance on a massive scale, making the challenge before us both clearer and more urgent.

CRUNCHING THE NUMBERS

Total finance for nature-based solutions reached US$220 billion in 2023. Public finance continues to do most of the heavy lifting, accounting for US$197 billion, or about 90% of the total. Private finance, by contrast, stood at just US$23.4 billion, underlining that the private capital is still not coming forward at the scale needed.

This is another worrying signal in the report. For years, much of the conversation has focused on how to crowd in more private capital, build investable pipelines, improve metrics and disclosures, and create the enabling conditions for finance to flow. But these latest figures suggest that, for all the progress in awareness and ambition, private participation is still fragile.

WHY THE SLOWDOWN?

The report does not offer a single simple answer, and neither should we. It would be easy to read the slowdown as proof that private interest in nature is fading. But the picture is more complicated than that.

On the one hand, private finance remains modest, and current flows are nowhere near what is needed. On the other hand, there are clear signs that awareness of nature-related risk is growing. UNEP notes that more than 730 organizations have now adopted the TNFD framework, representing US$22.4 trillion in assets under management. That suggests the issue is not one of visibility alone.

The challenge is turning growing awareness into actual capital allocation. That means confronting some hard realities. Nature finance is still often seen as difficult to structure, difficult to measure and difficult to scale. Policy signals are uneven. Public budgets are under pressure. And in a more uncertain global environment, investors may be retreating toward what feels familiar, even when the long-term risks of doing so are obvious.

WHAT HAPPENS NEXT?

There is still reason for cautious optimism. The financing gap is narrower than it was. We have better data than we did a few years ago. There is more recognition of nature-related risk across finance and business. And the report is clear that private capital could grow much faster with the right enabling conditions, standards and risk-sharing instruments in place.

But optimism alone will not close the gap. If the world is serious about reaching US$571 billion a year by 2030, then the next phase cannot rely on incremental growth alone. It will require a much more deliberate shift in how capital is directed.

That means, first, reducing the trillions still flowing into nature-negative activities. Even a small reallocation of harmful finance could dwarf current investment in nature-based solutions.

Second, it means making nature more investable. Better disclosures, more credible metrics and stronger pipelines all matter.

Third, it means de-risking private capital more effectively. Guarantees, blended finance and other public tools will remain essential if private finance is to scale.

And finally, it means policy clarity. Markets respond to signals. If governments want finance to move, they need to create the incentives, standards and frameworks that make that movement possible.

The latest UNEP figures do not tell a story of failure, but one of hesitation. With 2030 fast approaching, the critical question before us is whether governments, businesses and financial institutions can reverse this trend and act quickly enough to make that happen.